{kind=link}

Advisor Loans: SBA Versus Conventional Loan Programs

In years past advisors had to rely on personal assets, cash, and seller financing to buy equity or fund growth initiatives. Now financial advisors have greater access to capital through a variety of lenders who have entered the market. These new lending sources provide a wide range of options, all with different terms and requirements. Many of these loan programs fall under two categories: SBA and Conventional.

In recent years many conventional lenders have sought to undermine the value of SBA loan programs to financial advisors. As a government guaranty loan program, it does have certain criteria that must be met. However, SBA loans are also designed to provide credit to small businesses (including financial advisors) who might not otherwise have access to conventional funding sources. SBA loans also provide capital for asset purchases like real estate, which can become income generators on their own.

Each advisor and each situation are unique, so there is no situation where conventional always makes sense or when only an SBA loan makes sense. Still, it’s good for advisors to know and understand that different loan programs and when one or the other may be better for them.

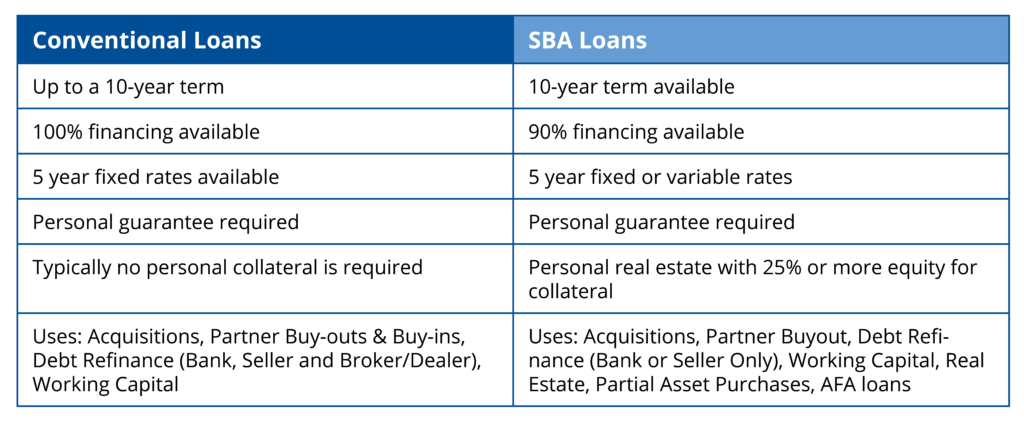

SBA Versus Conventional Loan Programs

The table below highlights the key elements of each loan program, including the basic terms and uses of proceeds.

At first glance, it may appear that conventional loan programs, which offer up to 100% financing and require no personal collateral, would be the preferred option for advisors. However, SBA loans often provide a lower interest rate compared to conventional loans and can give advisors who otherwise wouldn’t qualify for a conventional loan access to funds. For advisors with smaller practices or with little personal or business credit, SBA loans provide a path to ownership and growth that otherwise wouldn’t be available. Also, SBA loans are available for a broad range of uses including real estate.

One notable difference is that SBA loans cannot be used to refinance broker-dealer debt. Advisors who are looking to remove restrictive covenants tied to their broker-dealer loan will need to pursue a conventional loan. Also, SBA has some restrictions regarding partner buy-ins which must be structured as a partial asset purchase in order to meet SBA guidelines.

It’s important to note that not all lenders provide both SBA and conventional loans. Salt Creek is one of the few who has both loan programs under one roof. We also have established ourselves as a Preferred Lending Partner with the SBA, which also comes with additional benefits to a borrower, especially when timelines are an issue. If you have capital needs and would like to explore your loan options, schedule a free consultation with us now.

0 comments