SBA 7(a) vs. SBA 504 Loans: Key Differences and Parameters

When small businesses look to finance growth, working capital, or major purchases, two of the most popular options are the SBA 7(a) Loan Program and the SBA 504 Loan Program. Both are backed by the U.S. Small Business Administration (SBA), but they serve different purposes and have unique structures. Understanding these differences can help business owners choose the right financing tool for their needs.

At First State Bank Nebraska, we are proud to be a Preferred Lender with the SBA, which means faster decisions, streamlined processing, and expert guidance every step of the way.

SBA 7(a) Loan Program

Purpose

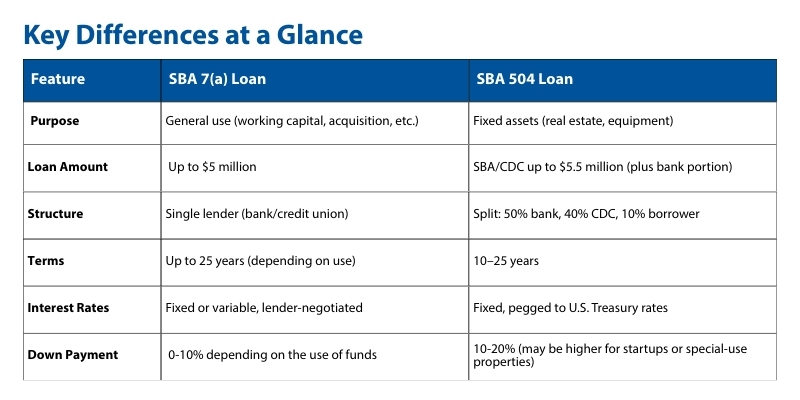

The SBA 7(a) loan is the most flexible SBA program, designed to cover a wide range of business needs.

Eligible Uses

- Working capital

- Business acquisition or partner buyout

- Refinancing certain types of debt

- Purchase of equipment, inventory, or supplies

- Real estate purchase (owner-occupied)

- Leasehold improvements

Loan Parameters

-

Maximum loan amount: $5 million

- Terms:

- Working capital/equipment: up to 10 years

- Real estate: up to 25 years

- Interest rates: Variable or fixed, negotiated between borrower and lender but capped by SBA

- Down payment: Often 0-10% depending on the use of funds

Best for: Businesses needing flexible financing for mixed purposes such as working capital, equipment, or business acquisition.

SBA 504 Loan Program

Purpose

The SBA 504 loan is a fixed-asset financing program that helps small businesses invest in long-term growth through property or equipment purchases. It’s structured differently than the 7(a) loan, involving a partnership between a Certified Development Company (CDC), a bank, and the borrower.

Eligible Uses

-

Purchase of land or existing buildings

- Construction of new facilities

- Long-term machinery or equipment

- Improvements or modernization of facilities

- Refinancing of eligible fixed assets

Loan Parameters

-

Maximum loan amount: Typically up to $5.5 million from the SBA/CDC portion (no official overall limit, since bank financing adds more)

- Loan structure:

- 50% from a bank or credit union

- 40% from a CDC (backed by the SBA)

- 10-20% down payment (may be higher for startups or special-use properties)

- Terms: 10, 20, or 25 years

- Interest rates: Fixed, tied to U.S. Treasury rates for the CDC portion

- Collateral: Primarily the asset being financed

Best for: Businesses planning large, long-term investments in real estate or major equipment, especially when they want predictable payments and lower down payments.

vs. SBA 504 Loans: Key Differences and Parameters&url=https://www.1fsb.bank/blog/post/sba-key-differences-and-parameters){kind=link}

Partner With First State Bank Nebraska

At First State Bank Nebraska, our SBA team is committed to helping local businesses grow and thrive. As a Preferred SBA Lender, we have the experience to get your loan processed efficiently—so you can focus on running your business.

Ready to get started? Click here to learn more about SBA loans at First State Bank Nebraska and connect with our lending team today.

0 comments